Should Physicians Incorporate?

Incorporation is the single biggest financial lever we get in this career. I learned absolutely nothing about it in medical school, residency, or fellowship. Sucks to suck — but right now, it’s on you to close that gap. Procrastination in this area can easily cost you tens of thousands of dollars in years of lost compounding.

What Incorporation Is

A Professional Corporation (PC) is a business structure through which you earn your clinical income. Instead of the Ministry or hospital depositing your payment directly into your personal bank account, it goes to your company. You then pay yourself from your company.

The power of incorporation is tax deferral. A dollar taxed later is almost always more valuable than a dollar taxed now, because deferral buys you more time in the market and more compounding. Incorporation also allows you to shift the timing of tax to a future year when you may be in a lower tax bracket (maternity or paternity leave, caregiver leave, leaving your current place of work, changing to part-time, moving to a new location, a sabbatical, retirement).

Without incorporation: Every dollar is taxed at your personal marginal rate (often 48–53% for physicians).

With incorporation: Your corporation pays tax at the small business rate (~12% depending on province).

The massive spread between 12% vs. 53% now is what creates the fuel (and time) for compounding. The CRA will (and always) gets paid eventually, but your corp (if structured and invested optimally) allows you to be taxed on a much bigger asset base that only exists because of the deferral. Always remember “time in the market beats timing the market”.

A subtle but essential concept at work here is tax integration, a core principle of the Canadian tax system. The goal is that a dollar earned through a corporation and paid out to you personally attracts roughly the same total tax as if you had just earned it personally in the first place. When a dollar is paid out of a corporation to an individual, the combined corporate tax + personal tax should roughly equal the tax that same dollar would have faced if it had been earned personally in the first place. Integration equalizes the final tax, but incorporation supercharges everything that happens before the final tax because deferral lets your money compound for years at the tiny corporate tax rate. Another way of thinking about it is like the RRSP, which is a personal tax deferral system. A corporation achieves the same underlying mechanism as an RRSP, but with two massive differences: There’s no contribution limit 🤯 + The tax rate inside the corp is dramatically lower than even RRSP deferral gives you 😱 (although once active business income exceeds $500k annually, the corporate tax rate increases to ~26%).

So, what is the point of incorporation?

Earn through your corporation

Retain earnings at a tax low rate

Invest those retained earnings

Withdraw strategically in lower-income years

Let the difference compound for as long as possible

The point is to control the timing, and timing is everything in a progressive tax system.

When Should a Physician Incorporate?

The right time to incorporate depends on several factors, and is generally worth considering when these conditions are met:

You have predictable staff income. Locums are fine as long as you plan to work consistently.

You have a 3–6 month emergency fund

You’ve maxed TFSA, RRSP, FHSA (Your personal tax shelters are more powerful and should be prioritized. See this post for how to prioritize them!)

You’ve paid off high-interest debt.

Credit cards are a non-negotiable to pay off.

Student LOC at Prime – 0.25%? Consider paying it down gradually — it’s cheap money.

You have meaningful surplus to invest.

If you spend everything you earn, incorporation does nothing

Anecdotally, I frequently hear/read that you need to retain $50K a year to make incorporation worthwhile. My actual setup and maintenance costs run under $10K, so I’m not sure who invented this rule. If I had to guess, they probably also think avocado toast is why millennials can’t buy houses. I believe the OG logic was that incorporation has fixed annual costs (lawyer, accountant, bookkeeping). If you retain too little income in the corp, fees consume the advantage. Therefore: “don’t bother unless you can retain $50K.” But that was when incorporation and bookkeeping cost way more and passive investment options were worse. Now, I think the costs are closer to ~$5–10K:

Setting up a PC with a lawyer: ~$2–5K once

Annual accounting/bookkeeping: ~$3–5K

Ongoing admin: trivial

Investment platforms: cheap (Wealthsimple, Questrade, IBKR)

The real threshold is simple: if you earn more than you spend, and that surplus exceeds your corporate admin costs, incorporation pays off

Practicalities

You need:

a lawyer (PC setup)

an accountant (corporate + personal taxes)

potentially a fee-for-service planner

That’s about ~$5–10K upfront + ~$2–4K per year.

During fellowship and early staff life, I lurked aggressively in finance forums and physician groups before choosing a lawyer, and most indispensably, an accountant. We interviewed a few, picked someone excellent, and incorporated immediately. I cannot stress this enough: Do not pick someone because a colleague said “they’re great.” Many of your colleagues have not optimized their finances. Do your own research, take nothing at face value, and find someone competent.

Common Myths About Incorporation

❌ “It’s not worth the cost.” It is if your savings rate is high enough.

❌ “Wait until after you buy a house.” This advice assumes buying a primary residence is the logical next step after graduating residency, which is often financially shortsighted. Plus, this advice usually comes from people who bought an expensive primary residence and are now spiritually committed to justifying the decision. Buying a home is a lifestyle choice, not a wealth-building strategy.

❌ “Pay off all debt first.” You absolutely should pay high-interest debt. Low interest? Consider paying over time.

❌ “My accountant can figure it out later.” Fine, but know that later may result in tens of thousands of dollars in lost opportunity cost. Incorporation strategy is front-loaded, not back-loaded. Missed opportunities (e.g., not opening the corp early, not retaining earnings, poor dividend/salary planning) cannot be retroactively fixed. Accountants can’t go back in time and un-tax money or generate lost compounding time from your highest-earning years.

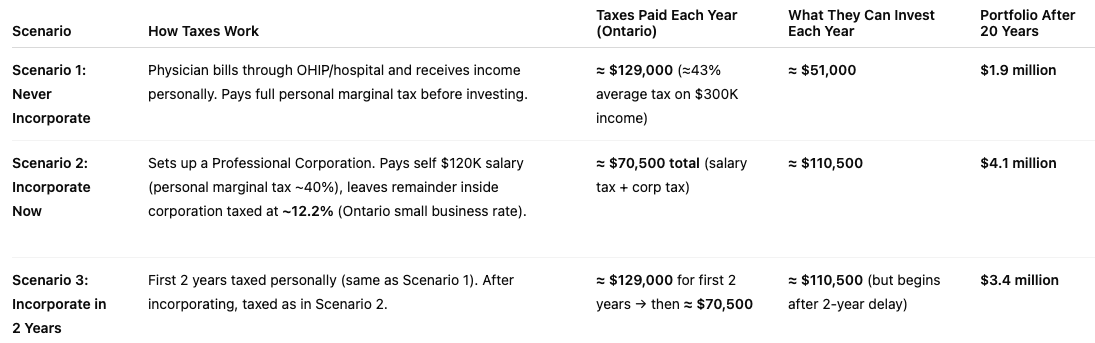

How Much Does Incorporation Timing Matter? A Lot.

Assumptions:

Both individuals earn $300K annually and spend $120K annually (Ontario resident).

All surplus cash is invested in low-cost, globally diversified index funds with an assumed 6% nominal annual return, compounded annually.

Corporate tax rate: 12.2–12.5% (Ontario small business rate, rounded to 12.5%).

Personal average tax rate: ≈43% on $300K salary income.

CPP/EI contributions, RRSP/TFSA/FHSA strategies, investment fees, and passive corporate income rules are excluded for simplicity.

Key Takeaways for Canadian Doctors

Incorporation is the biggest financial engine in your career.

You need predictable income + personal tax shelters maxed + meaningful savings first.

If those conditions are met and you are procrastinating incorporation, waiting costs money you cannot get back.

Don’t rely on colleagues for financial guidance — rely on competence.

Your corporation can become a multi-million-dollar investment engine in under a decade if you structure it optimally and invest smartly.

Which Accounts Should Physicians in Training Prioritize?

It all begins with an idea.

If you’re a medical student or resident in Canada, figuring out which financial accounts to open first (TFSA, RRSP, FHSA, or a simple high-interest savings account) can feel overwhelming. This guide breaks down exactly which accounts Canadian physicians in training should prioritize, why they matter, and how each one fits into your long-term wealth strategy.

Residency is financially restrictive: low income, high stress, irregular shifts, zero energy. This is the window where tiny, boring decisions snowball into massive advantages later and where you can set up structures that will make your future attending-self very grateful.

As a medical student and resident, I could not have told you what the acronyms RRSP, FHSA, or TFSA even stood for, let alone which one mattered. I genuinely thought that stowing away some cash in a TFSA meant it was “invested.” I didn’t understand contribution room, tax brackets, compounding, or why deferring RRSP deductions could unlock thousands of dollars later etc. I was too busy surviving 28-hour calls and trying not to cry during post-call rounds 💀. If this is you right now - exhausted, underpaid, and dangerously close to financial autopilot - you’re exactly who this post is for. You don’t need to become an expert. You just need to know which accounts matter, in what order, and why.

The Accounts Every Resident Should Know: Chequing, Savings, TFSA, RRSP, FHSA, RESP

Think of every financial account you have at your disposition as petri dishes. Each dish can contain money, but only some can grow money.

Chequing account:

This is a petri dish with no nutrients. Your money just sits there. It doesn’t grow. It doesn’t reproduce. It might even shrink in real terms because inflation quietly eats its value. Chequing is for paying bills and making transactions.Savings account:

This dish has a tiny bit of nutrient gel — enough for your money to grow by 0.5–2% per year if you’re lucky, which is still below inflation most years. It’s fine for short-term savings (emergency fund, car repair next month), but it is not an investing account. Money “saved” here does not become wealth.TFSA (Tax-Free Savings Account):

Misleading name…it should have been called the Tax-Free Investing Account. It’s a petri dish full of rich nutrients. You can use money within this petri dish to buy investments (aka securities aka assets aka financial instruments) and hold them inside the dish. This includes things like index funds (a grouping of stocks or bonds), ETFs (a type of index fund), stocks, bonds, and mutual funds. All the growth, dividends, and withdrawals are completely tax-free. This is one of the most powerful tools for residents because you’re likely in your late twenties/early thirties and have years to grow and compound your growth within this account without future tax obligations.RRSP (Registered Retirement Savings Plan):

Another nutrient-rich dish, but with very specific rules. You can opt for a tax deduction when filing your annual taxes, meaning the amount you put into the RRSP will be subtracted from your annual taxable income and this may knock you into a lower tax bracket and reduce the tax you owe. If you choose not to claim the deduction, you can do so in a future year.The money inside this account grows tax-deferred. So, unlike the TFSA (and FHSA when used properly for a first home) where you will never have to pay taxes on earnings upon withdrawal, you WILL have to pay taxes upon withdrawal of both contributions AND earnings with the RRSP. In essence, the RRSP allows you to simultaneously stow away some of your annual income and defer the taxes you would have paid on that income until you withdraw the money in the future.

FHSA (First Home Savings Account):

Think of this as a hybrid dish: RRSP-like deduction on the way in and tax-free growth and withdrawals like the TFSA if used on the down payment for your first home. For most residents who plan to buy a home within 5–15 years, the FHSA is a no-brainer.PRO TIP: If you intend to buy your first home within 15 years of reading this - open the FHSA even if you can’t put a dollar into it yet. FHSA contribution room only starts building after the account exists. It does not accrue retroactively like the TFSA.

If you wait until you’re a staff physician to open it, you’ll still get the $40,000 lifetime limit eventually… but you’ll be stuck contributing only $8,000 per year. That compromises your ability to front-load contributions (and the flexibility to claim the deduction in a high-income year when it’s actually worth something).

If you open it early, you build multiple years of room while earning resident money. Then, once you’re making your staff salary, you can dump in $16k, $24k, $32k, or the full $40k at once and claim the deduction when it’s most valuable. You can also defer the deduction until a high-income year.

RESP (Registered Education Savings Plan):

This is a petri dish you won’t use in residency unless you have kids. Think of the RESP as a dish that not only has nutrients, but an outside source (the government) adding more every time you contribute. For every dollar you put in, the government will top you up with 20% (the CESG, Canadian Education Savings Grant), up to $500 per year, per child. Also a misleading name; it is best used as an investing accounts, not a savings account. The growth inside is tax-sheltered. When your child eventually withdraws the funds for school, they’ll pay the tax; Because students have very low income, the tax is usually zero or close to it.There is a recurring cultural delusion that “good parents” must martyr themselves financially and shovel money into an RESP before they’ve saved a single dollar for their own retirement. Parents will talk about maxing their kid’s RESP while carrying consumer debt and having no investments of their own, as if it’s some sort of noble sacrifice. It’s not noble. It’s bad math.

The truth is:

Your child can get loans, grants, bursaries, scholarships for their education.

You cannot borrow to fund your retirement.

Your kids do not want to fund your retirement (or feel guilty about being unable to). The greatest financial gift you can give your children is being financially secure/informed while they’re young and not becoming a financial burden when they’re older.

Use the RESP strategically, not emotionally. For most families, the smart move is simply contributing $2,500 per year to capture the full government match. Do not put money into an RESP unless your own TFSA, FHSA, and RRSP strategy is already solid.

Your financial life is not about “opening accounts,” it’s about choosing which petri dishes to grow your money in. Most will not be able to max out any single one of these accounts…that is expected and normal. What matters is learning what each account represents and how they can make whatever amount you can set aside work for you.

The list

1. TFSA (Tax-Free Savings Account)

Annual contribution limit for 2025: $7,000. Your personal lifetime total depends on how many years have passed since you turned 18, and accumulates even if you have never opened a TFSA account.

Best for: low income years (medical school, residency, fellowship), predictable high future income (staff/attending), flexibility, tax-free growth

Your TFSA is the most valuable account during training:

You’re in a low tax bracket, so you’re not giving up much by not filling as RRSP and claiming deductions yet.

Growth inside a TFSA is completely tax-free forever.

You can use it for graduation moves, an emergency fund, a home down payment, or leave it invested for decades.

You can withdraw anytime, for anything: an emergency fund, a move, a down payment, or future investments.

If you do nothing else in residency, contribute to your TFSA.

2. Open an FHSA (First Home Savings Account) — even if you can’t fund it yet

Best for: future home buyers, tax deductions + tax-free growth

Maximum annual contribution: $8,000 per year. Lifetime maximum: $40,000. Unused annual room starts accumulating only once you open the account. Funds must be withdrawn for a qualifying first-home purchase within 15 years of opening the FHSA; otherwise, the full balance is rolled into your RRSP or RRIF tax-deferred (no longer tax-free).

The FHSA is great for residents because it combines the strengths of the TFSA and RRSP:

You get an RRSP-style deduction now or later

Your money grows tax-free like a TFSA if it is withdrawn for your first home

If you never buy a home, you can roll it into your RRSP tax-free

Question: “But I’m in a low tax bracket — should I claim the deduction?”

Answer: Do not claim the deduction now. Open and contribute, but save the deduction for when you’re a staff physician in a high tax bracket.

3. Contribute to Your RRSP (But Do Not Claim the Deduction Yet)

Best for: future tax optimization, using low-income years strategically.

Maximum annual contribution: 18% of the previous year’s earned income, up to a cap of $32,490 (2025 limit). Unused room accumulates automatically, whether or not you’ve opened an RRSP. When you make a contribution, you may claim it as a tax deduction in that year or defer the deduction to a future year.

RRSP deductions are most valuable when your income is high. So as a resident:

You can contribute to an RRSP and start to grow and invest that contribution, but you should almost never claim the deduction until you’re a staff physician.

Carry the deductions forward, allowing them to accumulate and use them in a future tax year when you’re in the highest marginal tax bracket, similar to deductions arising from contributions to the FHSA.

4. RESP (Registered Education Savings Plan)

Best for: future children’s education, government grants, long-term tax-efficient growth.

RESP contributions are not tax-deductible.

Money inside grows tax-deferred, not tax-free; grants and earnings are taxed in the student’s hands later (usually minimal).

The real value is the CESG: the government gives you 20% on the first $2,500 contributed each year (up to $500/year per child, lifetime CESG $7,200).

As a resident:

Do not put money into an RESP unless your own TFSA, FHSA, and RRSP strategies are already solid.

When you are ready, contribute $2,500 per child per year to get the full 20% match.

5. After-Tax (Non-Registered) Investing

Most residents are not in a position to invest beyond the accounts reviewed above. If you are, good for you.

Consider opening a non-registered account with a bank or brokerage, knowing that interest and foreign dividends are taxed at your full marginal tax rate, while capital gains and Canadian dividends receive more favourable tax treatment.

Putting It All Together

Yearly priority list:

Fill TFSA, open FHSA

Fund FHSA (do not claim the deduction yet)

Fund RRSP (do not claim the deduction yet)

Fund RESP up to $2500 per child per year

Fund Non-registered account

Once you become staff and your marginal tax rate jumps, consider claiming all deferred RRSP/FHSA deductions at once to generate a large tax refund or lower your tax burden.

Intro

It all begins with an idea.

Bitchmark Index is a Canadian physician personal finance blog created for women in medicine who want clear, practical education and guidance on money. If you’ve ever felt overwhelmed by investing, incorporation, taxes, or simply understanding how to build wealth as a doctor in Canada, this space is for you.

I’m a physician in my mid-thirties. So is my partner. Our household net worth is $1.45 million and our household income is $900-950,000 per year. We bring home equal portions.

I started working at fourteen in retail, camps, service jobs. Grants, scholarships, and debt got me through university. I then worked in the corporate world for a of couple years, and subsequently returned to school for medicine. My obsession with financial independence didn’t really ignite until residency: those years of underpaid labour, collapsing systems, and COVID-era chaos. Turns out exploitation is a fantastic catalyst for becoming an incisive bitch with a balance sheet.

I was lucky, too. I grew up in a major Canadian city with good public schools and social support. I’m white-passing. I met the right partner, early. I had “right time, right place” in ways that mattered.

My partner and I save anywhere more than $500k annually into our corporation. Just over 80% of our total net-work is invested in globally diversified low cost index funds. Assuming a conservative 4–5% in real returns, we are on track to reach about $10M net-worth within the next decade.

I find those numbers hard to believe, and while I’m incredibly grateful for my current position and place of privilege, gratitude and humility aren’t the point of this blog. I am striving for more and trying to understand how I can continue to push my financial position and make money work for me. I want to optimize, to sharpen, to keep building. I’m a self-taught personal finance girlie because, deep down, I’m competitive and relentless. I hated feeling helpless at tax time. I cringed hearing “my husband/dad handles that.” I hated watching women portrayed as financial bimbos who shop while the “real adults” manage money. I am also deeply motivated by a desire to seek vengeance on my parents’ crueler, more limited lives.

I taught myself the language of money, and I’m still learning what wealth really means socially, politically, personally. I am rich, but I want to be wealthy. And, I want you to be, too. If you’re an incisive bitch and you’re a high-earner that wants to learn more about how to make money work for you - this blog is for you!

I am not here to please you or to reassure you, so leave if you’re not ready to read what will likely come across as a smug, privileged woman’s takes on money and life. Thanks for reading Bitchmark Index!