Should Physicians Incorporate?

Incorporation is the single biggest financial lever we get in this career. I learned absolutely nothing about it in medical school, residency, or fellowship. Sucks to suck — but right now, it’s on you to close that gap. Procrastination in this area can easily cost you tens of thousands of dollars in years of lost compounding.

What Incorporation Is

A Professional Corporation (PC) is a business structure through which you earn your clinical income. Instead of the Ministry or hospital depositing your payment directly into your personal bank account, it goes to your company. You then pay yourself from your company.

The power of incorporation is tax deferral. A dollar taxed later is almost always more valuable than a dollar taxed now, because deferral buys you more time in the market and more compounding. Incorporation also allows you to shift the timing of tax to a future year when you may be in a lower tax bracket (maternity or paternity leave, caregiver leave, leaving your current place of work, changing to part-time, moving to a new location, a sabbatical, retirement).

Without incorporation: Every dollar is taxed at your personal marginal rate (often 48–53% for physicians).

With incorporation: Your corporation pays tax at the small business rate (~12% depending on province).

The massive spread between 12% vs. 53% now is what creates the fuel (and time) for compounding. The CRA will (and always) gets paid eventually, but your corp (if structured and invested optimally) allows you to be taxed on a much bigger asset base that only exists because of the deferral. Always remember “time in the market beats timing the market”.

A subtle but essential concept at work here is tax integration, a core principle of the Canadian tax system. The goal is that a dollar earned through a corporation and paid out to you personally attracts roughly the same total tax as if you had just earned it personally in the first place. When a dollar is paid out of a corporation to an individual, the combined corporate tax + personal tax should roughly equal the tax that same dollar would have faced if it had been earned personally in the first place. Integration equalizes the final tax, but incorporation supercharges everything that happens before the final tax because deferral lets your money compound for years at the tiny corporate tax rate. Another way of thinking about it is like the RRSP, which is a personal tax deferral system. A corporation achieves the same underlying mechanism as an RRSP, but with two massive differences: There’s no contribution limit 🤯 + The tax rate inside the corp is dramatically lower than even RRSP deferral gives you 😱 (although once active business income exceeds $500k annually, the corporate tax rate increases to ~26%).

So, what is the point of incorporation?

Earn through your corporation

Retain earnings at a tax low rate

Invest those retained earnings

Withdraw strategically in lower-income years

Let the difference compound for as long as possible

The point is to control the timing, and timing is everything in a progressive tax system.

When Should a Physician Incorporate?

The right time to incorporate depends on several factors, and is generally worth considering when these conditions are met:

You have predictable staff income. Locums are fine as long as you plan to work consistently.

You have a 3–6 month emergency fund

You’ve maxed TFSA, RRSP, FHSA (Your personal tax shelters are more powerful and should be prioritized. See this post for how to prioritize them!)

You’ve paid off high-interest debt.

Credit cards are a non-negotiable to pay off.

Student LOC at Prime – 0.25%? Consider paying it down gradually — it’s cheap money.

You have meaningful surplus to invest.

If you spend everything you earn, incorporation does nothing

Anecdotally, I frequently hear/read that you need to retain $50K a year to make incorporation worthwhile. My actual setup and maintenance costs run under $10K, so I’m not sure who invented this rule. If I had to guess, they probably also think avocado toast is why millennials can’t buy houses. I believe the OG logic was that incorporation has fixed annual costs (lawyer, accountant, bookkeeping). If you retain too little income in the corp, fees consume the advantage. Therefore: “don’t bother unless you can retain $50K.” But that was when incorporation and bookkeeping cost way more and passive investment options were worse. Now, I think the costs are closer to ~$5–10K:

Setting up a PC with a lawyer: ~$2–5K once

Annual accounting/bookkeeping: ~$3–5K

Ongoing admin: trivial

Investment platforms: cheap (Wealthsimple, Questrade, IBKR)

The real threshold is simple: if you earn more than you spend, and that surplus exceeds your corporate admin costs, incorporation pays off

Practicalities

You need:

a lawyer (PC setup)

an accountant (corporate + personal taxes)

potentially a fee-for-service planner

That’s about ~$5–10K upfront + ~$2–4K per year.

During fellowship and early staff life, I lurked aggressively in finance forums and physician groups before choosing a lawyer, and most indispensably, an accountant. We interviewed a few, picked someone excellent, and incorporated immediately. I cannot stress this enough: Do not pick someone because a colleague said “they’re great.” Many of your colleagues have not optimized their finances. Do your own research, take nothing at face value, and find someone competent.

Common Myths About Incorporation

❌ “It’s not worth the cost.” It is if your savings rate is high enough.

❌ “Wait until after you buy a house.” This advice assumes buying a primary residence is the logical next step after graduating residency, which is often financially shortsighted. Plus, this advice usually comes from people who bought an expensive primary residence and are now spiritually committed to justifying the decision. Buying a home is a lifestyle choice, not a wealth-building strategy.

❌ “Pay off all debt first.” You absolutely should pay high-interest debt. Low interest? Consider paying over time.

❌ “My accountant can figure it out later.” Fine, but know that later may result in tens of thousands of dollars in lost opportunity cost. Incorporation strategy is front-loaded, not back-loaded. Missed opportunities (e.g., not opening the corp early, not retaining earnings, poor dividend/salary planning) cannot be retroactively fixed. Accountants can’t go back in time and un-tax money or generate lost compounding time from your highest-earning years.

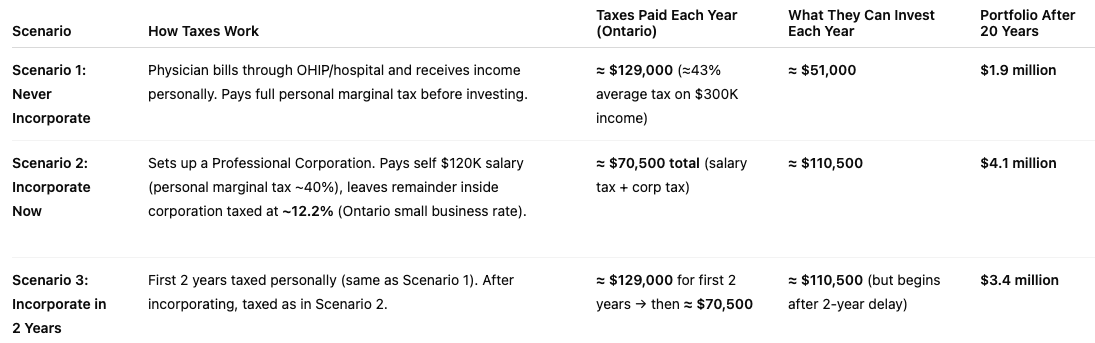

How Much Does Incorporation Timing Matter? A Lot.

Assumptions:

Both individuals earn $300K annually and spend $120K annually (Ontario resident).

All surplus cash is invested in low-cost, globally diversified index funds with an assumed 6% nominal annual return, compounded annually.

Corporate tax rate: 12.2–12.5% (Ontario small business rate, rounded to 12.5%).

Personal average tax rate: ≈43% on $300K salary income.

CPP/EI contributions, RRSP/TFSA/FHSA strategies, investment fees, and passive corporate income rules are excluded for simplicity.

Key Takeaways for Canadian Doctors

Incorporation is the biggest financial engine in your career.

You need predictable income + personal tax shelters maxed + meaningful savings first.

If those conditions are met and you are procrastinating incorporation, waiting costs money you cannot get back.

Don’t rely on colleagues for financial guidance — rely on competence.

Your corporation can become a multi-million-dollar investment engine in under a decade if you structure it optimally and invest smartly.